DeFi Weekly #58

DeFi Weekly #58

Debt is Coming (Fairmint and the Alt-STO Thesis), Convexity Protocol launches (I'm bearish due to peer-to-peer model), DeFi Hits $1B AUM (What it means and how it could accelerate future growth)

It seems that as we go by the weeks, there's so much more to unpack and keep a hold of in the DeFi world.

Buckle up!

Debt Financing and Fairmint. Recently, Alex Danco wrote a piece called "Debt is Coming" where he proposes that the next boom in Silicon Valley will be from cash-flow generating startups converting their future revenues into a debt offering for investors rather than continually diluting equity. The advantages of doing so are two fold:

Startups can use the revenues from one successful cash flow to finance the development or their next product without diluting ownership stakes and giving up control. It also reduces the mis-alignment between venture capital fund lifecycles and company priorities.

The pool of investors who are willing and able to purchase these newly created debt instruments is much larger and familiar to investors outside of venture capital (debt is how you grow)

How does this related to DeFi? Well, it was only just a week ago when Fairmint launched their new product that allows startups to securitise their debt via Ethereum on-chain. In the context of this article, what they're doing makes a lot of sense. The founder, Thibauld wrote about it in his tweet storm below which you can get additional context from:

Stepping back for a second though, it seems like that the approach to securitising the revenues rather than the entire company is much more intelligent and offers far more value compared to the traditional STO thesis every I-just-got-into-crypto-and-have-a-legal-background person shills. The liquidity for a token which offers cash flows over a period of time can tap into a global pool of liquidity much easier. I'd argue that LEO is the first instance of this working out (except they don't pay interest haha), as shown through the price graph shown below ($1 peg maintained but also some speculation).

As an engineer, my first thought is what their go-to market is since the hesitation to securitise revenues is risky, but then using crypto could be perceived as double risky. On top of this, there's hesitation from traditional VCs with this approach as shown through Fred Wilson's post written back in 2017 - https://avc.com/2017/03/using-debt-like-growth-equity/. It's hard to make any sort of conclusions at this point, but the trend suggests that a startup's capital stack has increasingly more options than just raising equity. Debt is risky but so is equity (it just hides risk much better).

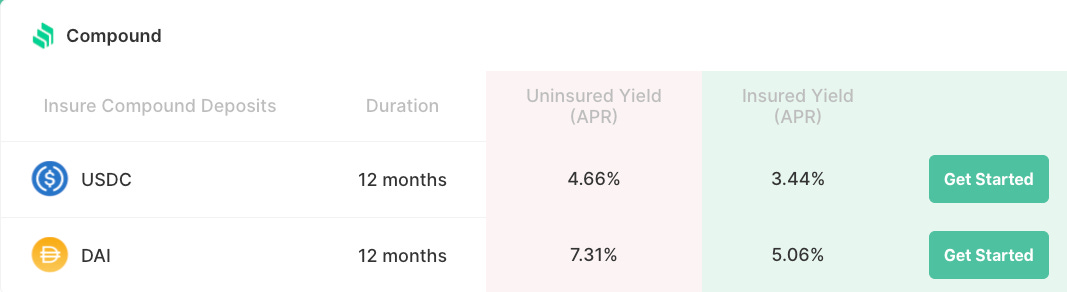

Convexity Protocol launches on main-net! For those of you who missed the announcement a while ago, Convexity is essentially a protocol for options trading with the first use case optimised around insurance for DeFi. An example that's commonly cited by the team is someone can purchase oDAI from an insurer at a premium of $1.02 which will give them the right to redeem the oDAI for USDC should DAI fail. In order to mint oDAI, the insurer will have to lock up 1 USDC (or a bit more to over collateralise but depends).

The product by the team using Convexity is actually Opyn, previously known for their leverage platform that utilised Uniswap and a few other protocol under the hood. After failing to find product market fit this is the team's second approach to the DeFi market. Overall it seems like a great move in the right direction to create a new DeFi primitive but the thing which makes me the most bearish about it is the peer-to-peer model of it rather than an contract-to-peer model (not sure how something like this). It's a minor difference but it really prevents protocols from achieving liquidity in the early phases especially. My prime example of this is Dharma v2 which relied on a similar peer-to-peer model for lenders and borrowers requiring the same preferences. Convexity has reduced this slightly by only splitting by asset and expiry time for their initial options but the point still stands that peer-to-peer models outside of DEXs struggle to establish meaningful two sided marketplaces. Their contracts have been audited and there's been a bit of liquidity added to the pool which signals they've probably raised a small bit of money to test the waters with this product.

Apart from the mechanics of the protocol, there's not much to the sustainability of the team's business model as there's been close to no token engineering to incentivise adoption of the protocol. It's probably deliberate to keep it as simple as possible and avoid regulatory concerns but still an opportunity missed on the table. Something like Convexity, from a product perspective, still seems too early for its time unless they can figure out a way to make the counter party for the options a pooled smart contract. Good luck to the team for the long road ahead and actually launching something that we can play around with!

You've obviously heart about it before but I wanted to cover another angle about DeFi hitting $1b locked up and what it possibly means in a wider context. Firstly, it's incredible to see that in just under 2 years there's been this much demand and growth for an industry during a crypto bear market. If you look at anyone new in the crypto space, DeFi is THE thing everyone naturally gravitates to since the value proposition is easy to understand, how it provides value and super easy to contribute in some form. From an investor perspective, it's a solid milestone that Ethereum has found product market fit in a primitive form and the growth of this movement can improve the fundamental assessment of Ethereum as an asset class. Criticisms around the trusted nature of oracles and backdoors still exist but it's easy to see a path in where those are slowly eliminated and these financial primitives become battle-tested infrastructure for many more billions to rely on.

If there's one area which has really caused DeFi to grow, it's easily been the rise of synthetic asset creation. First with MakerDAO and secondly with Synthetix with their recent run-up. What makes them both unique is that they have tokens that can allow anyone in the community to become a financial stakeholder in their success. Outside of synthetic asset generation, money markets come in second place with Compound and dYdX taking good chunk of volume. AMM such as Uniswap are highly interesting and have seen extreme growth but still aren't in the $100m+ AUM league. In my estimate I'd say that after the next bull run, we'll see primitives such as AMM DEXs and Pooled Money Markets really take off and the next set of primitives scaling to be 10x bigger than they are right now. Convexity might find more meaningful traction in this view of the world than the one we're in right now.

Another unmentioned aspect of DeFi hitting $1b locked up is that traction begets more traction, just like liquidity begets more liquidity. Just over the past month or two alone we've seen new products and protocols go live such as Aave, Curve, IEarn and more gaining traction quicker than I would have expected. With the number in DeFi continually going up, this space will continually get more and more interesting.