The New Age of Stablecoins

The New Age of Stablecoins

Understanding the new stablecoin models and how they work

Hey all, given the recent interest into stablecoins and their ever growing complex mechanics I thought I’d write a piece explaining how all of them work and what powers them.

The Core Insight

Behind all of these new generation stablecoins, there’s one key insight which all of them rely on: the only thing that matters for a stablecoin is how well it can maintain $1 parity. Over the past year especially, we saw MakerDAO despite being 150%+ collateralised, failed to maintain an accurate peg.

Why would a coin which has tons of collateral backing it fail to maintain its peg? The short answer is the forces of supply and demand apply to everything including so called “$1” coins. So really, what all of these new stablecoins attempt to do is balance out the forces of supply and demand through their own unique ways. What’s fascinating to see is that the idea is rapidly evolving and each model iterates on the one prior to it.

1. Ampleforth

This was the first algorithmic stablecoin to come out with the concept of rebasing to balance supply and demand. So the idea here is that when the price of AMPL goes above $1, the protocol will distribute/inflate everyone’s balance so that they have more AMPL and each AMPL is worth $1 now. Here’s an example straight from their website:

Alice has 1 AMPL in her wallet worth 1$USD. The demand for AMPL suddenly rises, and the market price for AMPL jumps to 2$USD.

The Ampleforth protocol adjusts supply, and now Alice has 2 AMPL worth 1$USD each. What is remarkable about Ampleforth is that it is non-dilutive, meaning that Alice will still have in her wallet the same percentage of Ampleforth’s total supply when it changes.The key thing which Ampleforth prides itself on is the fact that its non-dilutive meaning despite more AMPL being created/destroyed, your raw percentage ownership never changes. However one of the major problems with AMPL is that it breaks anything it integrates into. Why? Because they modify the supply of the ERC20 token in a non-compliant way. As a result, AMPL isn’t very useful throughout DeFi and can cause a lot of problems to be used as anything beyond speculative games. Furthermore, AMPL has a set of early investors that purchased AMPL at much lower valuations than the intended $1 which means that the stablecoin itself is a wealth game for early adopters. As we’ll see, this isn’t exclusive to just Ampleforth.

The key tenant of algorithmic stablecoins is that once they grow large enough, their volatility is dampened and they can become proper $1 coins. However as we see from the above, there is very little evidence of the mean/average price of AMPL restoring back the $1 peg with less volatile swings.

2. ESD

I wrote about ESD in November last year as it improved on the Ampleforth model, however since then we’ve learned some pretty important lessons. For those of you that aren’t aware of how ESD works I’ll quickly summarise it below. ESD is an improvement on Ampleforth in the fact it adjusts the supply by guiding market participants to do what it wants.

When ESD is trading at a premium, those who have “locked” up their tokens receive more ESD when the price of ESD goes above $1. Easy enough to solve. This is what causes sell pressure when the peg trades at a premium.

When ESD is trading at a discount, anyone who purchases ESD on the open market can then lock their ESD to earn coupons. Coupons give a share of the the newly minted ESD during a positive rebase. This is what causes buy pressure when the peg trades at a discount. The lower the price of ESD, the higher the discount.

If that feels to brief for you to understand, here are some resources on learning more:

Now on to the core piece here, ESD has done phenomenally well at attracting and creating a community with some smart people through the fact the project started as an “anonymous developer” who launched the protocol by themselves and created a “fair launch” sort of mechanic (this isn’t completely true though).

How’s it done? Well it was doing pretty well up until the last expansion phase where ESD was offering 1000%+ returns to investors and attracted a lot of attention. As a result the market cap grew from $300m to $550m over the course of a few days. Such growth was obviously unsustainable and as a result ESD has been in downwards death spiral reaching as low as $0.30. Whether investors feel confident again in driving the price up or another algorithmic stablcoin speculative mania is to be seen.

The ESD community isn’t sitting idle of course, they’re currently working on ESD v2 with the core difference being that the protocol itself will store some sort of reserve which can be used to buy ESD on the open market to drive the price back up to $1 if the price goes below. This reserve of USDC will be built by the ESD money printer selling ESD for USDC when above the peg. There’s still plenty to work out and lots in research but the second iteration of this money game will be interesting to see.

The core insight here is that while you can use speculation to bootstrap growth, transitioning to a phase of confidence and stability is very hard to achieve. While ESD managed to grow to a $0.5b market cap coin in a few short months, it wasn’t able to retain that status for too long. Ultimately speculation runs dry and when that happens you need something more to sell as a protocol apart from speculation.

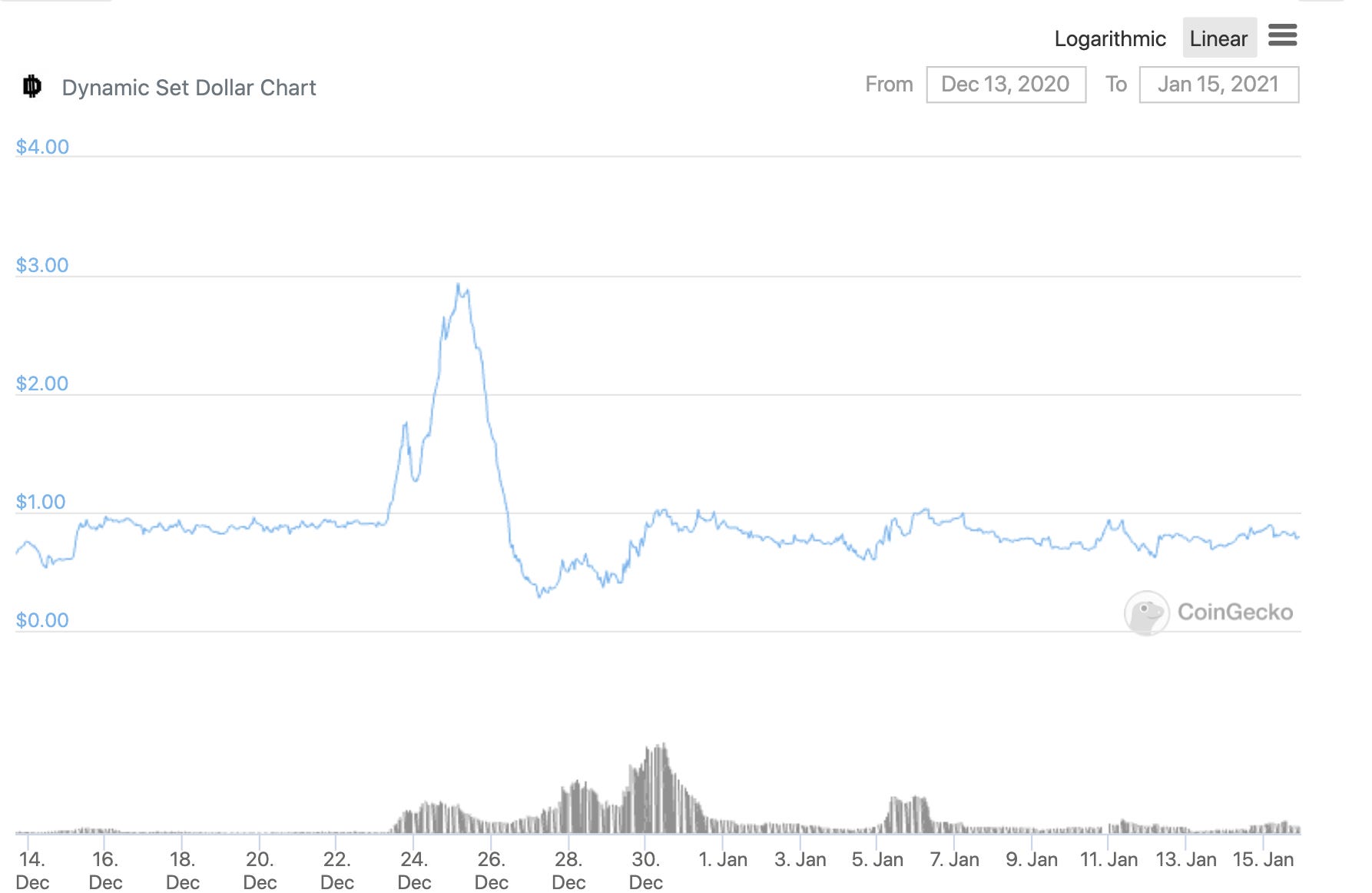

2.5. DSD

Excuse the awkward numbering but I wanted to bring up DSD since they provide some additional context as to other paths where confidence may be lost in the protocol. DSD is fork of ESD but is essentially sped up through shorter epochs. What this means is that whatever happens in ESD happens much faster in DSD.

Since DSD has been below peg for a while now, the number of outstanding coupons (they can be redeemed for real DSD when the price goes above $1) are set to expire in a few days. Given this deadline, a large holder of DSD was selling to offload his/her bags and causing prices to drop. In order to save DSD, a coalition of buyers came together in order to buy out the whale and stop the dumping:

Why did they do this? Well, when the price goes below $1 coupons (debt) is issued to help reduce supply on the market. Since these coupons have an expiry date, if the price continues to keep dropping then the coupons will expire and coupon holders lose money which causes a loss in faith and most likely a very brutal downwards spiral.

The key lesson here (and from ESD) is that you can’t keep selling future speculation for debt since you will eventually run out of buyers! The notion of a stablecoin backed by nothing is impossible to sustain since by definition speculation is a limited and unpredictable quantity - especially in the crypto space.

3. FRAX

The latest and somewhat strongest contender around the block as it offers something different other competitors don’t have: some sort of collateral base backing it. The FRAX model claims to be under-collateralised but rather a more accurate description is that it’s algorithmically collateralised through a two token system. Here’s how it works:

The system starts off being 100% collateral based, which means that in order to mint FRAX you need 1 USDC per FRAX. However, if this is anything below 100% then an equivalent amount of FXS (Frax Shares) need to be deposited. Think of it that rather than depositing 1 USDC you would deposit 0.9 USDC and $0.10 worth of FXS. It’s not really under-collateralized since you still need to deposit at least $1 of value, however it isn’t over-collateralized.

Now, as time goes on, if the price of FRAX is above $1, then the collateral ratio reduces by 0.25% each hour. If the price of FRAX is below $1 then the collateral ratio increases by 0.25% each hour.

The net result is that the system can become something like 90% collateralized meaning only 90% of USDC needs to be deposited and 10% of FXS per FRAX minted.

However, this isn’t what helps FRAX maintain its peg. The crucial part here is that anyone who buys and holds FRAX can redeem it for $1 worth of USDC and/or FXS. This means that the peg can be a lot stronger since arbitragers can buy cheap FRAX if it goes below $1 and redeem it for $1 of real collateral. Similarly if the price of FRAX goes above $1 then arbs can come in and mint 1 FRAX for $1 and then sell it for $1.10 (or whatever the above-peg price is).

While the FRAX model does move in the right direction, it still has a few major problems:

Right now FRAX only supports USDC meaning it’s a wrapped for USDC in some ways. FRAX v2 attempts to add volatile currencies through the introduction of FRAX bonds.

FRAX can’t be used effectively for leverage (like MakerDAO or ARCx) since depositors have no guarantee that they’ll receive their exact amount and type of collateral back. This may be okay assuming FRAX aims to be a primary MoE exchange coin. However, like others, the main beneficiaries of the FRAX stablecoin are the FXS holders who will have increasing power to mint FRAX with their FXS.

The last point around early holders is something I think that plagues all algorithmic stablecoins, and that’s the fact that they enrich early holders at the expense of later holders. Ultimately this will hinder their ability for real adoption since the late adopters will become the early adopter’s exit liquidity.

4. ARCx

While ARCx isn’t trying to be an algorithmic stablecoin, it attempts to take the learnings from all of the above to incorporate it into its model of a new stablecoin that can be productive by issuing credit against different or novel types of DeFi collateral. The thinking here is that can you incorporate algorithmic monetary policy to a credit issuance tool to create a new use-case altogether?

This is a fundamentally different model to the existing algostables out there as it serves a different purpose altogether of not being a speculation game but rather a way to unlock liquidity for a variety of assets. The future is a multiverse of stablecoins, not a winner takes all.

In our research so far we’ve narrowed down on three different levers to maintain the peg which we’ll be looking to test an iterate on in the coming weeks and months. Those levers are as follows:

Interest rate - the cost of borrowing/minting the stablecoin. Similar to most DeFi platforms out there.

Savings rate - a pure inflationary/seigniorage rate that is distributed to users who lock up their STABLEx (stablecoin) to the savings contract. In some sorts this acts as a negative interest rate to pay borrowers when the peg is trading at a premium or to encourage borrowing within the system.

System arbitrage - basically the protocol itself can mint STABLEx out of thin air and then sell for USDC to build up native reserves. These reserves can then be used to buy back STABLEx when it trades at a discount. It’s basically the protocol trading against the system participants itself to help maintain price parity.

As of now the STABLEx is peg is trading at a discount due to three reasons which are helpful to note as they confirm theories we all know about stablecoins so far.

The existing yield farming contract requires the LP provider to be the minter of the debt as well. Simply buying STABLEx from Uniswap and becoming an LP won’t work. We did this deliberately to encourage growth of STABLEx’s native supply and to test the basic premise of using idle assets to mint a stablecoin. However, it prevents “ape” behaviour which means that you’re running a dampened experiment. When we launched LINKUSD we experienced the opposite where the price went through the roof due to buyers of STABLEx farming ARCx.

While enforcing minters to be LPs promotes growth, it causes a problem where the incentive for users to re-pay debt when it goes below peg is broken since users will lose their ARCx rewards and get “slashed” - aka lose all their rewards. Yield farming incentives for synthetic assets often clash and protocol designers should be cautious.

Using a constant product curve such as Uniswap or Balancer will always yield in an unstable peg. We knew this after migrating LINKUSD (our first stablecoin) from Balancer to Curve. Stability is a function of the primary liquidity source’s algorithm. Many have discovered this in the past few weeks, expect more to migrate over in the coming weeks.

As we enable liquidity for the underlying ARCx token and enable these levers we’ll be sharing more!

Closing

While it’s easy to view all of these stablecoins at odds with each other, I actually believe that all of them can and should co-exist. Not all stablecoins are created equal and not all of them are intended for the same purpose either. Those who view stablecoins as cute gimmicks for now will be in for a ride as the meta-verse of stablecoins explodes beyond what we know.

I almost view it analogous to how people viewed “altcoins” when Bitcoin was around. Eventually in crypto, an explosion of tokens always happens and the infrastructure to support that explosion will emerge alongside it as well. Curve now has permissionless stablecoin pools which anyone can spin up and we’ll start seeing many more beginning to be spun up as people learn that constant product curves are terrible for stables.

If you find stablecoins interesting in general, I recently created a group called “Stablecoin Big Brains”. Let me know by replying to this or reaching out to me to get an invite :)

Coming TERRA stablecoin?

mSTABLE